Value-added tax, abbreviated as VAT, is a tax on final consumption. For most countries in the world, VAT is the main consumption tax, which is levied on the value added at each production and distribution step and then paid by the consumer.

VAT’s role should not be undervalued, as it is one of the primary revenue sources for many governments across the globe. For example, according to the European Commission, the contribution of VAT accounted for about 27% of the total yearly tax receipts for general government in the EU.

Because taxes are refunded on inputs, governments worldwide face taxpayer noncompliance with VAT payment obligations. This type of noncompliance, including all its forms from the legal exploitation of tax system loopholes to actual tax evasion and fraud, often becomes one of the main drivers of the VAT compliance gap.

Complex technology was developed to help governments combat VAT fraud, including e-invoicing and near real-time reporting solutions, such as traceCORE B2B E-Invoicing and Government Business Intelligence (BI). Read further to learn more about these systems and how they work, as well as about VAT and VAT fraud in general.

VAT as the Largest Source of Consumption Tax Revenues

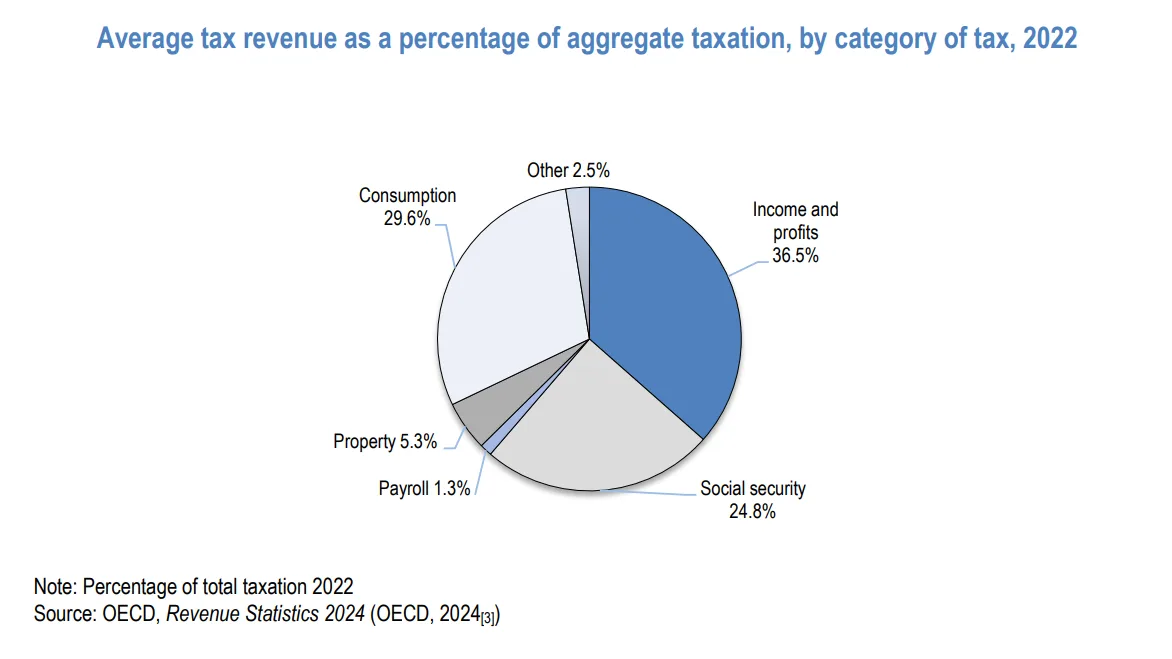

According to the Consumption Tax Trends 2024 report prepared by the OECD, consumption taxes accounted for 29.6% of the total tax revenue in OECD countries on average in 2022, which represents 9.9% of those countries’ GDP.

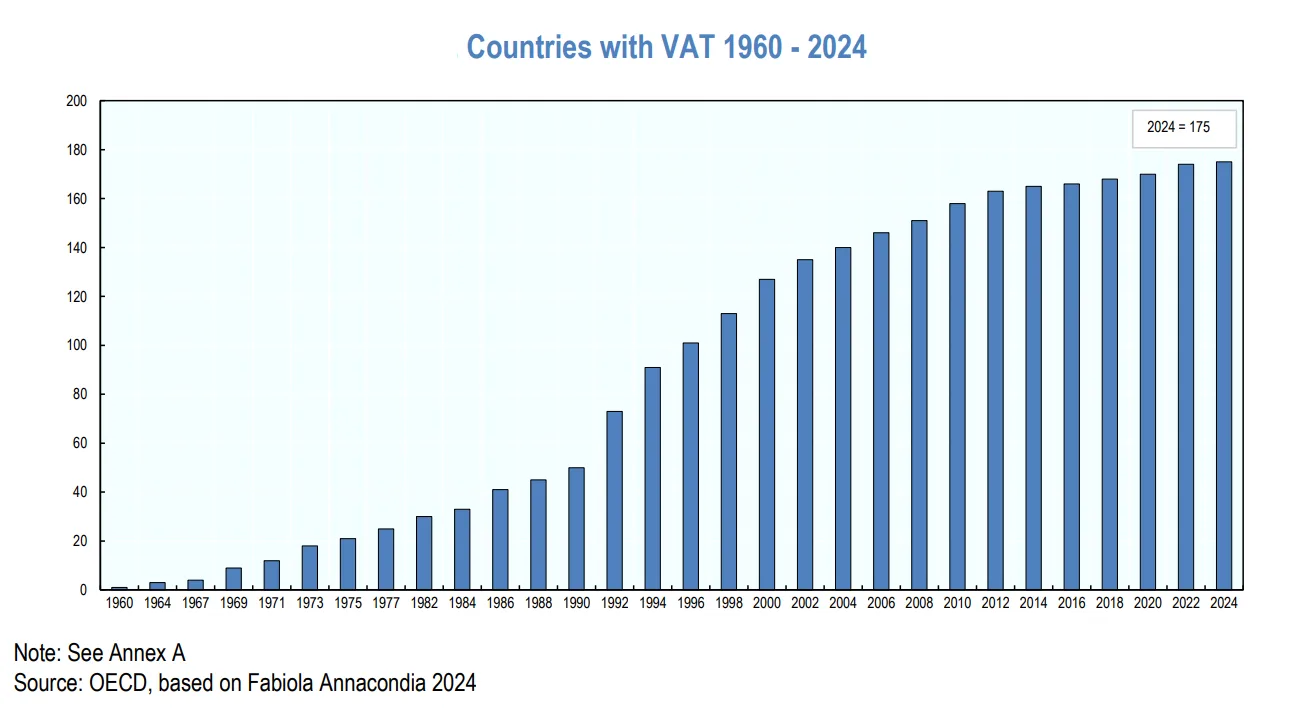

Due to tax policy decisions and the effective VAT collection by the tax system, VAT remains the largest source of consumption tax revenues. Since its adoption in several countries back in the late 1960s, VAT has transformed tax systems worldwide and become a significant revenue source in 175 countries. This success can be explained by the fact that VAT is rather neutral and effective when applied both domestically and internationally, especially compared to other forms of taxation.

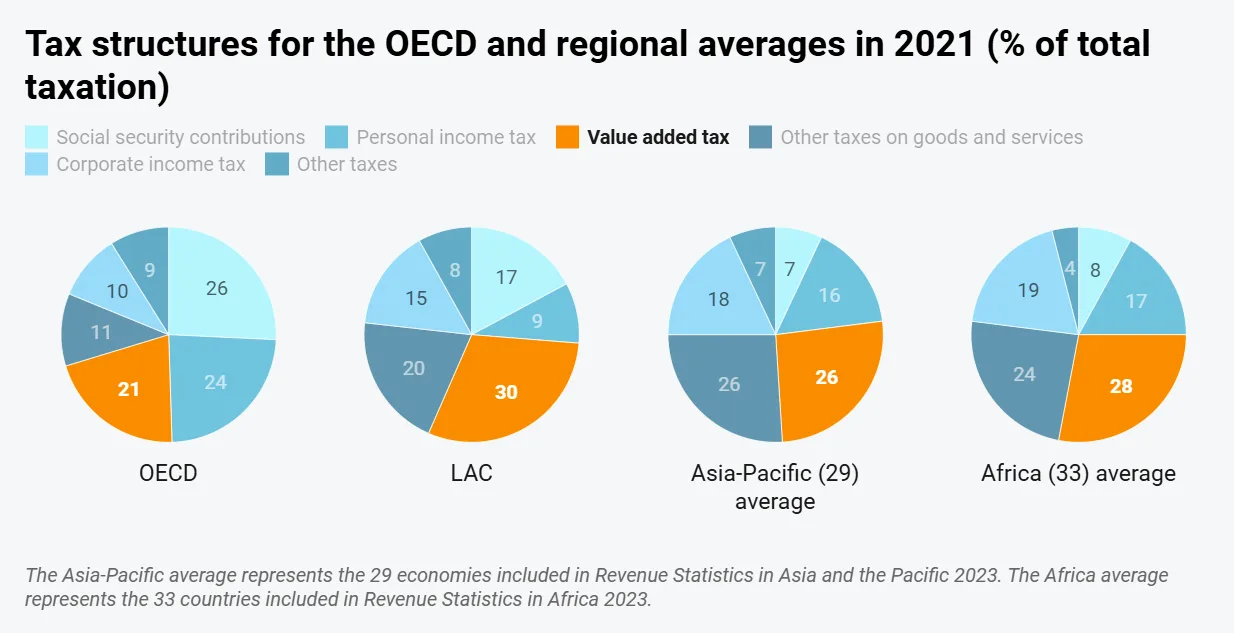

Moreover, VAT is often the largest part of tax revenue for developing countries, including those that have very low income in general. It accounts for a quarter or more of their total tax revenue. This is why governments should pay extra attention to VAT revenues in their countries and make sure to secure them.

Source: OECD, 2023. Global Revenue Statistics Database, https://www.oecd.org/en/data/datasets/global-revenue-statistics-database.html

Source: OECD, 2023. Global Revenue Statistics Database, https://www.oecd.org/en/data/datasets/global-revenue-statistics-database.html

With digital taxation tools by traceCORE, such as B2B E-Invoicing, it’s possible to increase VAT collection by up to 150%. Contact us to learn how we can help solve the VAT underreporting problem in your country.

Value-Added Tax (VAT) and Retail Sales Tax: What’s The Difference

While VAT is the most common general consumption tax worldwide, there is also another form of this tax: retail sales tax (RST). It is primarily used in the United States and varies from state to state.

RST is charged only once on products at the last point of sale to the end consumer. It means that only consumers have to pay the tax, and resellers are not charged if they are not final product users. This is why resellers have to provide sellers with “resale certificates” that prove that they are purchasing products to resell them or with “direct pay” permits that indicate that necessary tax obligations will be fulfilled. If buyers can’t provide such evidence, the tax is charged on each item sold to them. RST covers all businesses working with buyers who can’t provide any evidence proving that no tax is due, not just retailers.

The sales price is the basis for taxation. As it is with VAT, the tax burden can be calculated precisely and, in principle, there’s no discrimination between different production forms or distribution channels.

The outcomes of VAT and RST should be the same, as both of them aim to tax the final consumption of a wide product range where such consumption takes place. In addition, they both tax the transaction between the seller and the purchaser rather than the consumption itself. However, the result can often be different, considering the core difference in the way the tax is collected. When it comes to VAT, the tax is collected at each stage of the value chain under a staged payment system. RST is collected only at the very last stage — on the sale by the retailer to the end consumer.

The RST system has quite a few disadvantages: if the rate is high, small retailers have to face a lot of pressure. All the revenue is put at risk since the retailer can fail to remit the tax to the authorities. The audit and invoice trail is much weaker than under a VAT as well, especially when it comes to services. Moreover, revenue is not secured at the time of importation, which can be critical for developing countries. The conclusion is that a single point resale sales tax works well if rates are low, but challenges arise when the rates become higher.

VAT Avoidance vs. Evasion vs. Fraud

Because VAT is a key revenue source for governments worldwide, the revenues at risk from VAT noncompliance and fraud can be significant. This is why it’s crucial for countries to develop strategies that can reduce the vulnerability of VAT systems to VAT noncompliance and fraud, as well as to ensure that the associated revenue losses are limited.

The rapid growth of online trade has increased risks of VAT noncompliance and fraud, forcing governments around the globe to deal with a huge number of non-resident businesses that may have an increased economic activity within their territory. That led to unscrupulous individuals taking advantage of the situation and more instances of VAT noncompliance and fraud.

According to the 2023 Vat Gap report by the European Commission, the EU lost around €61 billion in VAT in 2021. It was estimated that one quarter of those losses happened due to VAT carousel fraud, evasion and avoidance. For that reason, the EU Member States’ budgets were reduced.

The Difference Between Tax Avoidance, Evasion, and Fraud

While people may have an idea of what kind of activities can be described as tax fraud, tax avoidance and tax evasion can sound synonymous. However, these legal terms mean very different things.

Tax Avoidance

Tax avoidance describes actions within the law that can often be on the verge of legality (but still legal) with the aim of reducing or eliminating tax that the taxpayer has to pay.

Tax Evasion

Tax evasion means illegal activity where tax liability is hidden or ignored: the situations when the taxpayer hides income or information from tax authorities to pay less tax than required.

Tax Fraud

Tax fraud is a form of deliberate tax evasion where the taxpayer submits false statements or fake documents on purpose, as well as engages in other fraudulent schemes.

Overall, the main difference between tax avoidance (unintentional noncompliance) and tax evasion, including tax fraud (intentional noncompliance) is that in the first case the taxpayer can be unaware of compliance obligations or unable to comply for a valid reason, while in the second case the taxpayer deliberately fails to meet VAT obligations in order to reduce or avoid VAT liability. When it comes to VAT fraud specifically, illegal activities are involved with the aim of stealing public money, including fake invoicing, carousel fraud, etc.

The Most Common Types of VAT Fraud

Carousel Fraud

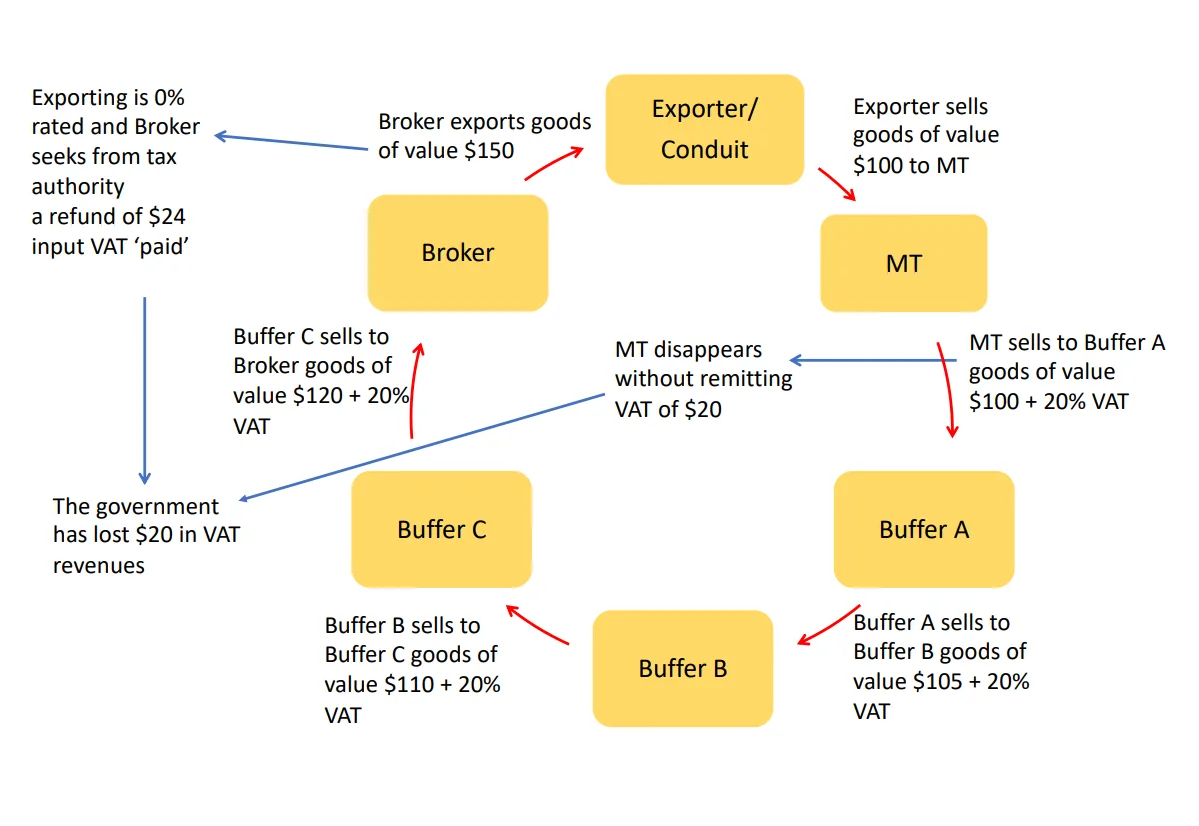

Also known as missing trader intra-community (MTIC) fraud, carousel fraud is a complex form of VAT fraud that creates numerous challenges for tax authorities and can cost governments billions annually in tax losses.

Carousel fraud is a scheme that involves a few interconnected companies abusing the VAT rules for cross-border transactions by avoiding VAT payments or by fraudulently claiming VAT refund from the government.

When it comes to this type of fraud, the schemes are built around high-value goods (often electronics) and manipulations with them across international borders in a circular way. Each participating company buys and sells the same items several times, but the only legitimate transaction is the initial one. The purpose of all the other transactions that come after that one is to create fraudulent VAT refund claims.

Contra-Trading Fraud

To make the detection of carousel fraud even more difficult for tax authorities, the participants of a scheme like that can resort to “contra-trading”.

Contra-trading involves using two carousels of purchased goods where one carousel is real, and the other one is fake. The contra-trader’s output tax from the first transaction chain is meant to off-set the input tax in the second chain.

There are two types of transaction chains:

Tax loss chains: The contra-trader incurs input tax on purchases made in Country A within the EU and then makes zero-rated supplies of those goods to consumers either in the EU or exports it abroad.

Contra chains: The contra-trader from Country A within the EU usually purchases goods from another EU Member State and sells them to businesses in Country A. In this case, the contra-trader acts as an acquirer and generates an output tax liability from the sale in Country A.

Missing Trader Fraud

In missing trader fraud, a business that is also known as a “missing” trader fraudulently claims a VAT refund on items supposedly bought for resale. But that business never actually gets or imports the goods.

Knowing that VAT is charged at each step of the supply chain and how VAT refund usually works, the missing trader uses that information with the intent to claim VAT refunds on fake transactions.

Acquisition Fraud

Acquisition fraud is a scheme that involves purchasing goods and services from another country and then selling it to the end consumer. The route the goods or services take often differs from the expected audit trail that can be indicated by invoices.

In acquisition fraud, there is a defaulter – the person who avoids their tax obligations – and buffers – fraud participants whose aim is to make it even more difficult for tax authorities to detect the scheme.

Cash Fraud

Cash fraud is a scheme that is created with the aim of avoiding paying the accurate VAT amount by underreporting sales transactions made in cash.

The participating companies deliberately fake their records to make it seem like there were fewer sales than they actually had in order to lower their VAT payments, thus keeping the portion of collected VAT that has to go to the government instead.

Online Fraud

Online fraud involves manipulating VAT systems and evading tax payments by exploiting the digital landscape.

In this scheme, the participants take advantage of the fact that online transactions can often be anonymous and complex, forcing tax authorities to face challenges when it comes to fraud detection and prevention.

Source: A. Alexopoulos, 2023. “A machine learning and network approach to Value Added Tax fraud detection”, illustration of the simplest case of the carousel VAT fraud, https://arxiv.org/pdf/2106.14005

Source: A. Alexopoulos, 2023. “A machine learning and network approach to Value Added Tax fraud detection”, illustration of the simplest case of the carousel VAT fraud, https://arxiv.org/pdf/2106.14005

How Governments Can Efficiently Detect VAT Fraud in the Digital Age

While the VAT Gap in the EU was estimated at €61 billion in 2021, a significant decline compared to previous years is quite obvious — it was €134 billion in 2019.

One of the key factors that contributed to this change became the implementation of digital reporting and effective audits. Due to the active digitalization of business accounting and invoicing, tax authorities and companies that work with them were able to develop new tools for detecting and combating VAT noncompliance and fraud. This approach is changing the nature of the tax compliance environment, making it more targeted and well-managed.

According to the OECD, the process of digitalization makes more tax-related data from taxpayers and third parties available to tax administrations, such as e-invoicing details, automated transaction data reporting, online cash registers and financial account information. That allows tax administrations to take action in a timely and more targeted manner.

Data analytics helps tax authorities automate tasks, streamline workflows and improve the accuracy and speed of their operations, thus reducing the need for manual intervention and minimizing errors.

OECD countries have been gradually switching from paper invoices or digitized invoices (for example, simple copies of invoices in PDF format) to real e-invoices. E-invoicing is now permitted in all OECD countries, although technical standards may vary from country to country. Moreover, almost all these countries have made e-invoicing compulsory for B2G supplies (i.e. between businesses and governments), some countries made it compulsory for even B2B (between businesses) and B2C (to end consumers) supplies.

In addition, to reduce the underreporting of B2C transactions, including those that involve cash payments, it’s highly recommended for governments to implement the mandatory use of electronic cash registers and secure software with unalterable memory.

Why Choose traceCORE B2B E-Invoicing and Government Business Intelligence (BI)

traceCORE B2B E-Invoicing is a digital solution that allows organizations to seamlessly exchange electronic invoices. E-invoice details are transmitted to the tax authority’s information system, and VAT is automatically accrued based on the provided data.

Mandatory B2B E-Invoicing is essential for implementing Continuous Transaction Controls (CTC) in the B2B segment. CTC are processes and technology that allow tax authorities to carry out seamless monitoring of financial transactions. It’s done by obtaining data directly from business transaction processes or data management systems, in the form of a dynamic business transaction ledger. To learn more about CTC, check out the following blog post: Approaches to E-Invoicing Implementation.

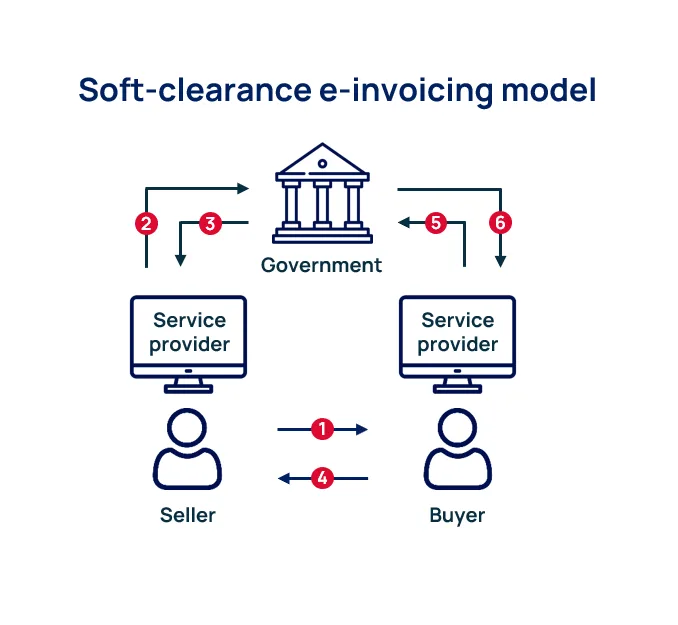

E-invoice exchange can be implemented via different models with varying degrees of the tax authority involvement.

We recommend implementing the soft clearance e-invoicing model, where e-invoice exchange occurs through a certified platform. Taxpayers can issue invoices either through this platform or through their ERP-systems that are integrated with the platform by API. In turn, tax authorities receive detailed information on invoice movement between counterparties through the platform.

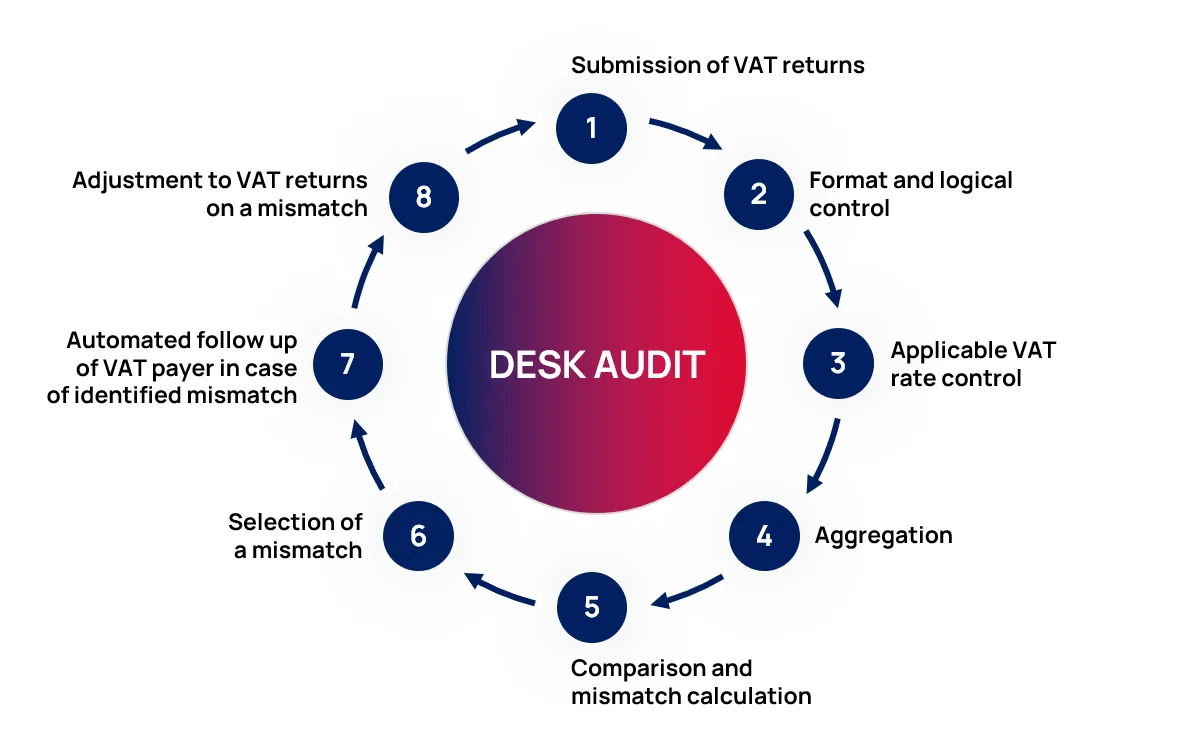

traceCORE B2B E-Invoicing also automates VAT returns control. Taxpayers submit VAT returns via a tax portal or from companies’ accounting software using APIs. The system double-checks VAT rates, aggregates the data and calculates the gaps. After that, taxpayers receive electronic claims for justification and then they either submit adjustments to VAT returns or provide justification.

VAT connections tree is one of the features inside traceCORE B2B E-Invoicing that helps identify VAT fraud schemes in manual or automatic mode. Its traceability function reveals the chains of matched transactions from the tax gap to the end beneficiary. The identified chains of related counterparties can be used to build taxpayers’ risk profiles as well as for further analysis.

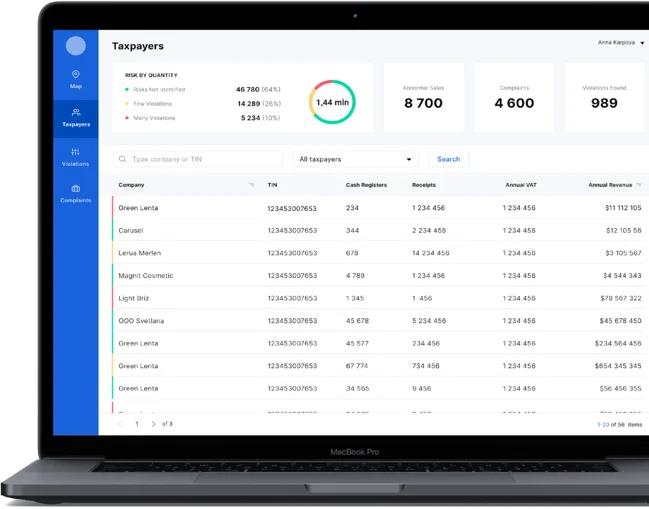

In addition, traceCORE Government Business Intelligence (BI) has AI tools for detecting and preventing VAT/GST fraud schemes. It’s a comprehensive solution for collecting, managing and analyzing big data on the country’s B2B and B2C transactions that works in near-real-time mode, collects and processes big data from every invoice, every receipt, every cash register, and every VAT taxpayer across the country.

After big data processing, the system creates visualizations, graphs and dashboards to enable users to investigate various data levels.

This solution is also used for advanced analytics, decision-making, modeling and forecasting. The system scores taxpayers and predicts their behavior with the help of machine learning. To learn more about using AI tools for governments, read the following post: How to Transform Tax Compliance Using AI-Powered Tax Software.

traceCORE Government BI can be integrated with B2B and B2C E-Invoicing solutions, tax authorities’ information systems, Fiscal Data Operator, and other sources of big data.

Conclusion

Nowadays, there are many complex VAT fraud schemes that are either very difficult or even close to impossible to detect using traditional methods without modern digital tools.

VAT fraud leads to significant compliance costs for legitimate VAT registered businesses that are required to ensure the legitimacy of their suppliers. Because of other individuals’ fraudulent actions, some of those legitimate businesses can even face bankruptcy. Consumers are also affected by VAT fraud, as this might result in a higher VAT gap and therefore higher VAT rates to compensate for lost tax revenue.

Implementing traceCORE digital taxation tools can help governments around the world decrease their VAT gap, automate a lot of routine tasks for tax authorities, and improve tax compliance.

Related Posts

All posts

How to Tackle Tax Fraud and Tax Evasion Using traceCORE Digital Desk Audit

In this post, we’re going to explore the benefits of traceCORE Digital Desk Audit, and how it offers a promising pathway to improve compliance, target abusive actors, and close revenue leaks before they grow into systemic shortfalls.