.webp)

To respond to the evolving digital landscape, governments are innovating to combat fraud and streamline their economies. One powerful tool is mandatory e-invoicing.

The e-invoicing initiative is a crucial step toward implementing continuous transaction controls. As government agencies closely monitor e-invoices from start to finish, they can leverage CTC (Continuous Transaction Controls) for real-time tax and data reporting.

State Goals with E-Invoicing Implementation

Implementing e-invoicing is essential for governments to meet crucial objectives.

Minimize the Tax Gap

E-invoicing helps in minimizing the tax gap, which is the disparity between owed and collected taxes.

By optimizing invoicing processes and creating a more efficient and equitable tax system, the state curbs revenue loss that comes from non-compliance.

Automate VAT Administration

E-invoicing simplifies value-added tax administration through automation, streamlining VAT collection and enabling tax authorities to better monitor transactions.

In turn, it improves transparency and accountability in VAT reporting.

Combat VAT Evasion

E-invoicing is essential in combating fraud schemes linked to VAT evasion. Electronic systems authenticate invoices, which helps governments detect irregularities more efficiently.

Such a proactive approach strengthens tax system integrity and promotes fair taxation.

Understanding Continuous Transaction Controls (CTC)

As explained by Pagero, continuous transaction controls (CTC) enable tax authorities to access real-time or near real time financial data from businesses in their countries.

It means that CTC tackles the inefficiencies that have long been associated with retroactive audits, where auditors access transaction data only after the fact, typically at an aggregated level. Traditional audits also depend on data stored and compiled by the businesses being audited.

CTC eliminates the reliance on historical evidence ledgers by enabling tax authorities to collect relevant information in the form of a dynamic business transaction ledger.

Where Does the Term Continuous Transaction Controls Come From?

Here's how the meaning behind the term CTC can be deciphered, according to Pagero:

-

"Continuous" means that the data is provided on a continuous basis, rather than at set intervals.

-

"Transaction" refers to invoices and other related documents, including orders, dispatch advices, and invoice responses.

-

"Controls" refers to equipping tax authorities with the solutions they need to reduce the potential for tax fraud.

What Is the Link Between E-Invoicing and CTC?

E-invoicing is used with many CTC models, while CTC frameworks are built on similar technologies and processes.

The key difference is that e-invoicing lacks the real-time control feature.

Despite that fact, government agencies often implement both together, that's why e-invoicing could be included in the term CTC.

Exploring Five E-Invoicing Models

E-invoice exchange can be implemented via different models with varying degrees of the tax authority involvement.

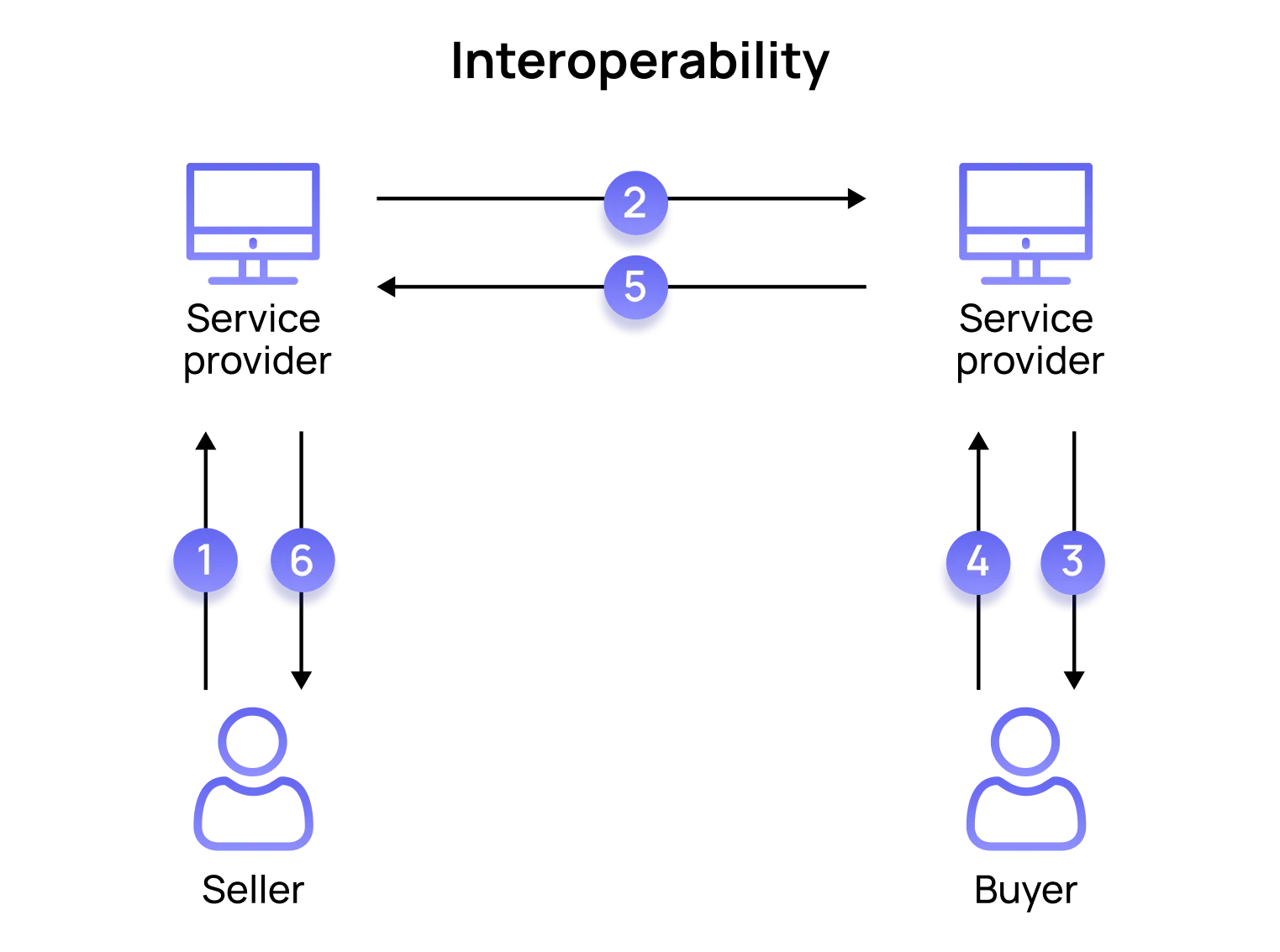

Interoperability Model

The interoperability model refers to a system where a network of private service providers adopts a unified and predefined document format and exchange methodology.

For example, Peppol (a widely used framework designed for the secure exchange of electronic business documents between trading parties, aiming to facilitate easy and secure e-document exchanges between entities across the globe) and Finland.

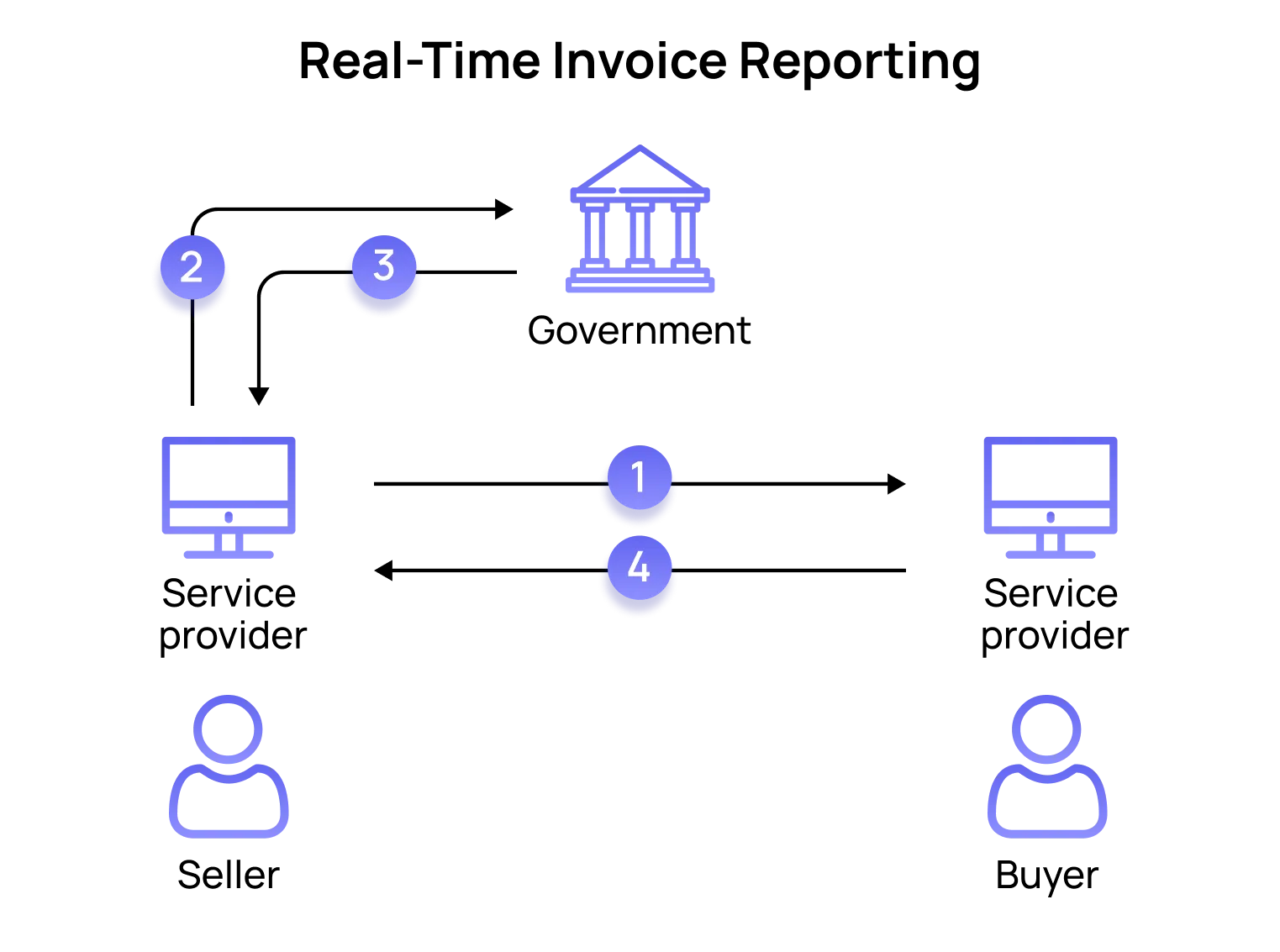

Real-Time Invoice Reporting Model

Real-time reporting refers to the process where, upon issuing an invoice, the relevant data is simultaneously transmitted to a government CTC platform.

For example, Hungary and South Korea.

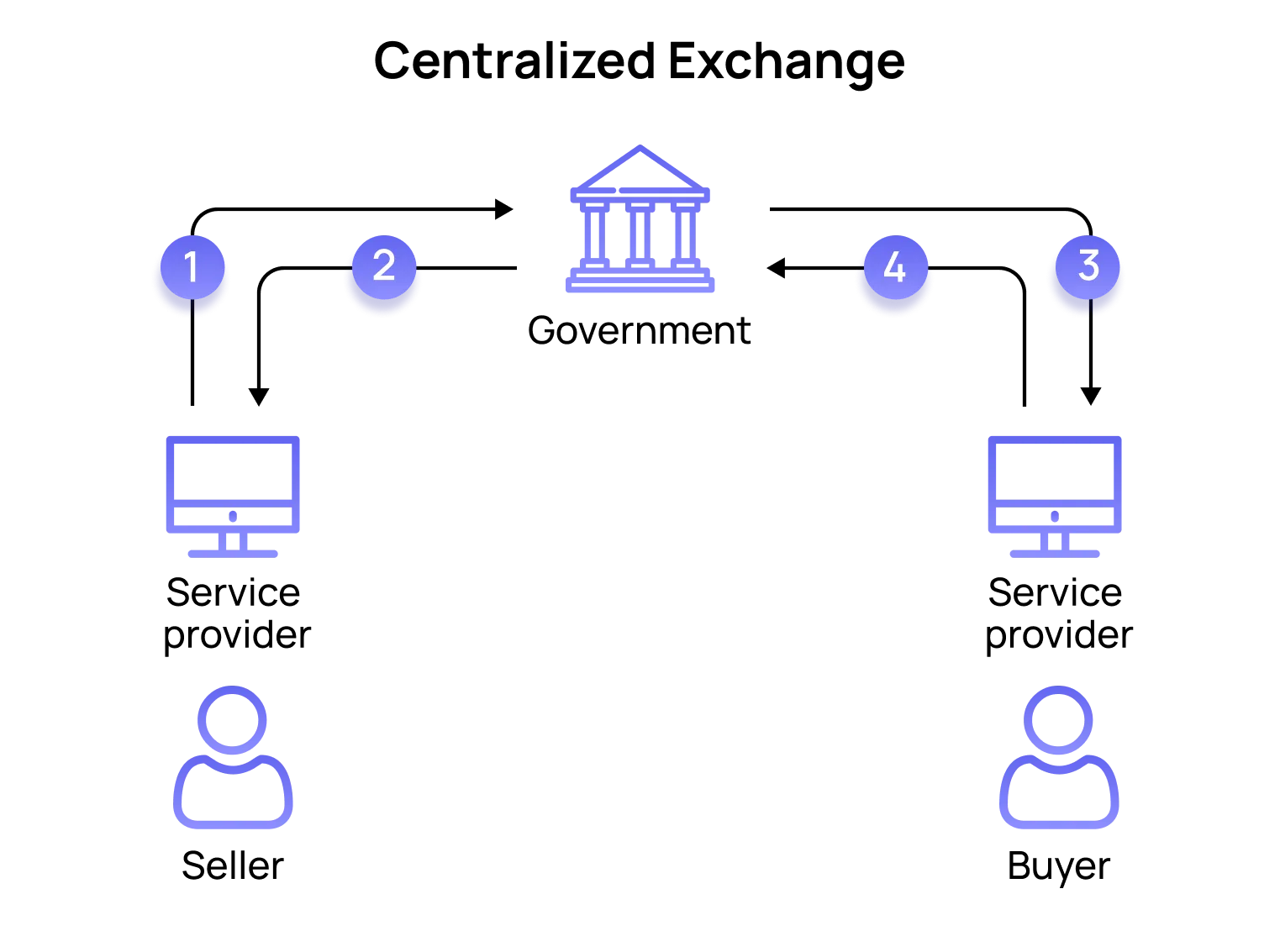

Centralized Exchange Model

This model restricts the direct exchange of regulated documents between trading parties. Instead, these documents must be issued through a government CTC platform.

For example, Italy and Turkey.

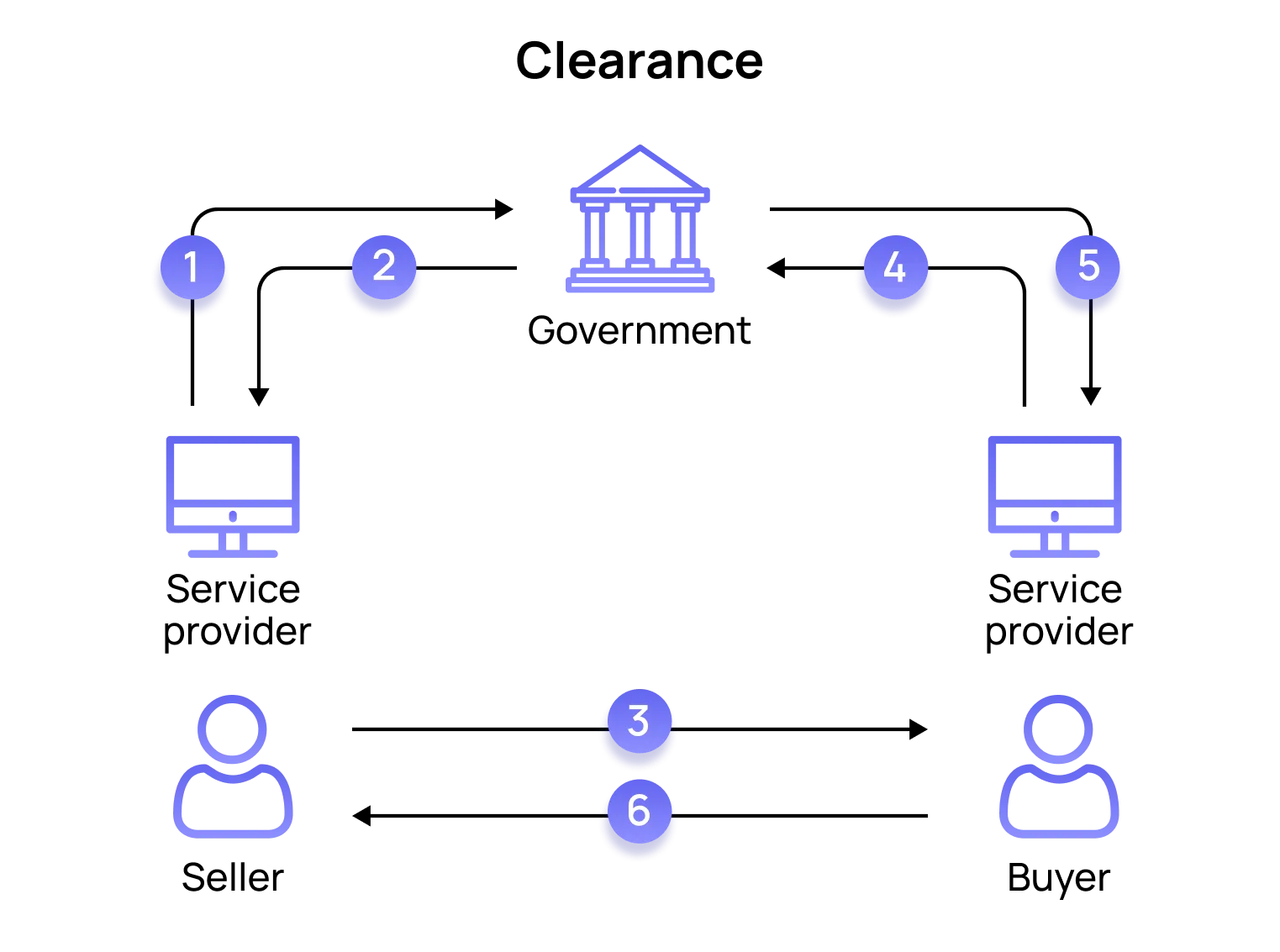

Clearance Model

A government CTC platform or certified service providers clear invoices before them being exchanged between the trading parties. After clearance, the seller sends the document directly to the buyer, who verifies its clearance.

There are several versions of this model. For example, Chile and Mexico.

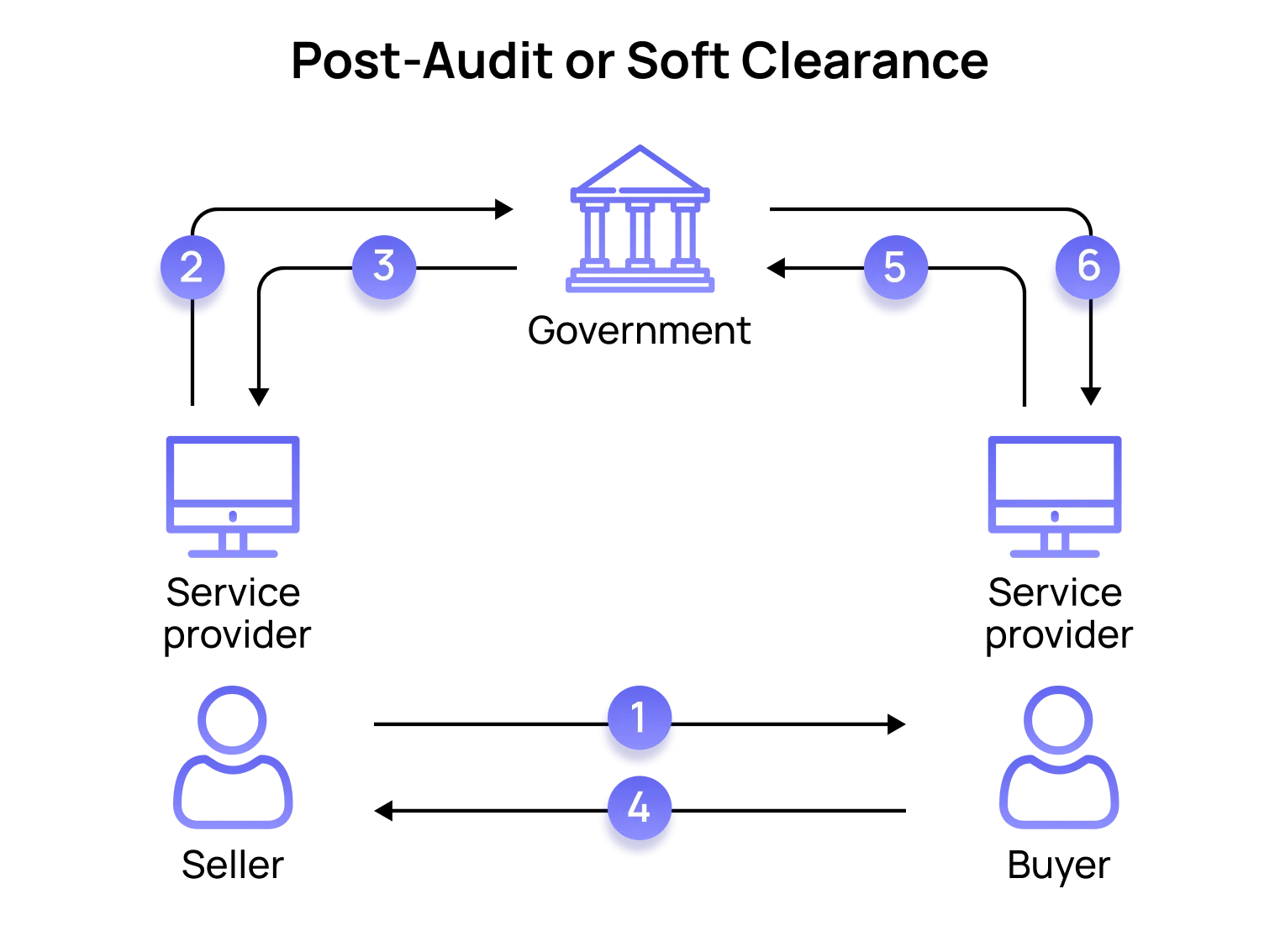

Post-Audit or Soft Clearance Model

Taxpayers exclusively utilize a certified platform for the exchange of VAT invoices.

Tax authorities periodically receive comprehensive information regarding invoice movement between counterparties through the platform.

This model is mainly used by European and Commonwealth countries.

Which E-invoicing Model Works Best?

Each e-invoicing model exists for a reason, as governments around the globe operate in different ways.

However, we recommend implementing the post-audit or soft clearance e-invoicing model. It's a flexible solution that is designed to optimize operating efficiency and tax compliance.

Unlike the Clearance model, the Post-Audit model doesn't require invoice clearance by a government CTC platform. However, the government still receives transaction information in near real time.

Pros of Having One Service Provider Instead of Many

If there's only one service provider, governments can ensure that they receive full and consistent data at all times. Such data is much easier to process and analyze, which helps detect any suspicious transactions and VAT fraud in a timely manner.

With just one trustworthy provider, governments save costs on implementation and have a lot more options when it comes to data analysis.

traceCORE B2B E-Invoicing is based on the Post-Audit or Soft Clearance model. To learn more about it and how it works, visit this page.

Why Choose traceCORE B2B E-Invoicing

Tax Evasion Prevention

traceCORE B2B E-Invoicing streamlines VAT administration processes and helps prevent tax evasion.

Automated Invoice Management

traceCORE B2B E-Invoicing automatically generates and transmits invoices from the supplier to the customer and to tax authorities.

Certified Platform Use

The post-audit or soft clearance e-invoicing model entails using a certified platform for the e-invoice exchange between organizations.

ERP System Integration

Taxpayers can issue and transfer invoices through the certified platform or through their ERP systems that are integrated with the platform by API.

Automatic VAT Accrual

VAT is automatically accrued and included in the e-invoice.

Tax Authority Monitoring

Tax authorities receive comprehensive information about B2B transactions and invoice movement between counterparties through the platform.

Conclusion

In summary, countries are continuing to implement new e-invoicing rules, and this trend is expected to grow. New proposals aim to create an operational environment that achieves both fiscal integrity and economic efficiency for everyone involved. That is why they are likely to receive significant support.

Governments around the world use various e-invoicing models, but the one that is recommended is the Post-Audit or Soft Clearance model. It helps save costs on the e-invoicing implementation, achieve better data consistency, and promptly detect suspicious transactions.

Related Posts

All posts

How to Tackle Tax Fraud and Tax Evasion Using traceCORE Digital Desk Audit

In this post, we’re going to explore the benefits of traceCORE Digital Desk Audit, and how it offers a promising pathway to improve compliance, target abusive actors, and close revenue leaks before they grow into systemic shortfalls.